From getting accurate data to responding to new regulatory challenges, there are plenty of opportunities and obstacles to overcome for RegTech innovators.

The RegTech sector has come into its own. Ever since the great recession of 2008, governments around the world have been clamouring to tighten up the legislation controlling the financial sector, looking to avoid another economic downturn. As more companies move to comply with the regulations, it has created opportunities for savvy RegTech entrepreneurs to establish enterprises to help them out.

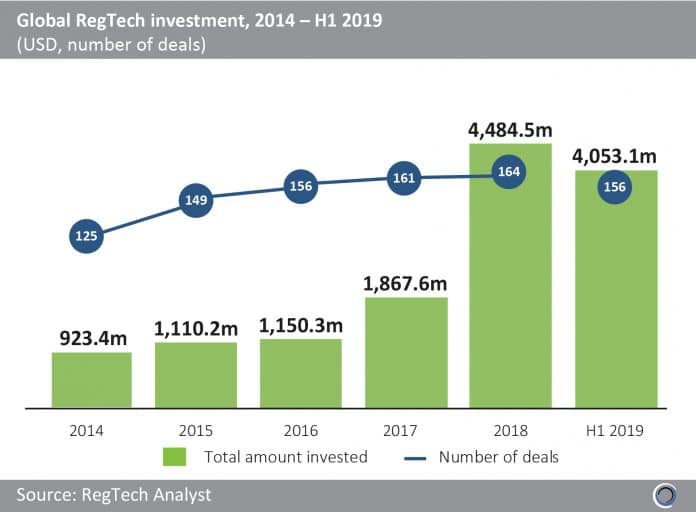

Investors also recognize the opportunities to make a killing. The investment in the sector jumped from $923.4m to $4.48bn between 2014 and 2018, according to RegTech Analyst’s research. In the first six months of 2019, the global RegTech sector attracted $4.05bn across 159 deals.

However, John Lee, president at Compliance Solutions Strategies (CSS), the RegTech company, believes smaller startups in the industry are struggling to find financial backers because there are too many companies looking to get rich out of RegTech. “The next stage of growth for RegTech will see existing providers investing in organic growth and thereby deepening their value proposition in order to meet new regulatory demands as they appear,” Lee tells RegTech Analyst.

“I think you’re going to see more investment taken on by the existing providers of RegTech as they look to support the regulatory compliance needs of their customers and in the process build deeper relationships. In return we’ll see the financial services industry look to consolidate vendor relationships, moving from single tactical providers into strategic partnerships with specialist compliance firms such as CSS.”

To make it even more challenging, many of the new entrepreneurs establishing enterprises on the back of the RegTech sector’s popularity are not really helping with compliance, according to Samuel Roberts, digital marketing manager at MirrorWeb, the company providing digital content compliance. Instead, he argues that many of them are simply trying to get traction by using the buzz around the industry.

“RegTech has become a significant area of growth in the tech space, with firms eager to satisfy their regulatory requirements and opting for an outsourcing model over developing this expertise in-house,” says Roberts. “However, some RegTech offerings provide little more than a skin-deep solution to regulatory requirements and lack the deeper knowledge or value a compliance professional could offer. Indeed, some opportunistic FinTech firms are simply calling themselves RegTech vendors. This not only brings scepticism onto this terminology but can make some cost-conscious firms question the role of outsourcing to vendors in general. “

And convincing customers to embrace the RegTech solutions is far from easy, according to Anthony Quinn, founder and CEO of Arctic Intelligence, the RegTech company specializing in anti-money-laundering (AML) compliance. “In spite of the encouragement regulators have given regulated entities to adopt RegTech solutions, the pace of adoption is still incredibly slow and the time to value is far too long,” he tells RegTech Analyst. “[This means] RegTech firms must play a patient game [as] having the best technology does not matter if organisations are not willing to embrace technology.”

Moreover, regulations themselves can prove a huge challenge for RegTech ventures. “Today’s compliance leaders are essentially drowning in information,” says Roberts. “To put that into context, it’s said that over 600 million documents will be produced in the next five years that are directly tied to regulation. With so many regulations to address they must have expert knowledge as to what each regulation is asking of them and then prioritize accordingly.”

For instance, EU’s Markets in Financial Instruments Directive (MiFID II), which is a set of rules so complicated that regulators reportedly spent 30,000 pages and 1.5 million paragraphs just to understand it.

“Regulation is also much more about interpretation, it’s no longer the box ticking exercise it used to be,” Roberts continues. “This means firms must focus on the actual outcomes of the requirements as opposed to just trying to meet them. This means a lack of deep knowledge.”

As an example, when MAP FinTech, the RegTech company focusing on ensuring compliant reporting, created its new tool for complying with MiFID II, the developers needed to both understand the letters of the law and meaning behind them. Understandably, this was both a challenging and time-consuming endeavour.

Even though regulations are half of the way RegTech companies’ category name, some enterprises may faulter due to an overemphasis on the second part. “A common pitfall of today’s RegTech vendors is that the technology doesn’t address regulatory needs,” Roberts suggests. “The vendors are more focused on the tech as opposed to examining the problem they’re trying to solve.”

This can prove particularly problematic as laws and regulations rarely exist in a vacuum but tend to be intimately intertwined. For instance, the General Data Protection Regulation (GDPR) is all about protecting private data whereas the revised Payment Service Directive (PSD2) is all about opening up data. Understandably toeing that line can prove a challenge. To add even more complexity, firms may operate in different jurisdictions and therefore be subjected to several different regulators.

“Therefore, compliance solutions need to be holistic in their approach,” Roberts suggests. “The most popular – and successful – RegTech vendors will be able to provide solutions for regulated firms’ entire compliance needs and not just segments of it.”

He adds, “Unfortunately, critics argue that many RegTech vendors lack a deeper understanding of the regulations due to their focus on the tech aspect of the solution. Therefore, RegTech vendors need to move beyond simple interpretation of these regulations and build a greater focus on outcomes into their solutions.“

Speaking of GDPR, it can also pose a serious headache for businesses operating on social media. “On top of the extensively regulated nature of their primary business activities, financial services firms have to contend with social media platforms which are posing an increasingly significant risk,” explains Roberts. “Not only is this because of the sheer amount and speed of data on these platforms, but also they are primarily used by individuals which therefore has grave connotations for GDPR and financial promotion risks. These social media platforms and how they are used pose an unavoidable regulatory risk for firms which will demand greater compliance resources over time.”

Data can also prove to be a concern in other ways. “The biggest challenge facing the RegTech sector today is getting accurate data, with auditable provenance in a timely way,” says Thomas Russell, founder and managing director of Think Evolve Solve, the RegTech firm providing businesses with actionable data insights. “There is an insatiable demand for data from multiple disparate sources, internal and external, but in a regulated environment the quality and accuracy of that data needs to be validated, controlled and managed. For the most, regulators, investors and other stakeholders have welcomed the use of data tools for reporting, planning and analysis.

“However, we are seeing an increasing demand for organisations across the financial services industry to evidence the validity and control of their data. As the sector continues to build new systems and solutions for clients, it needs to own this challenge and provide clients with the knowledge and tools to prove data quality. That’s how we will deliver on the promise of RegTech.”

Copyright © 2019 RegTech Analyst

Read the original article at here.